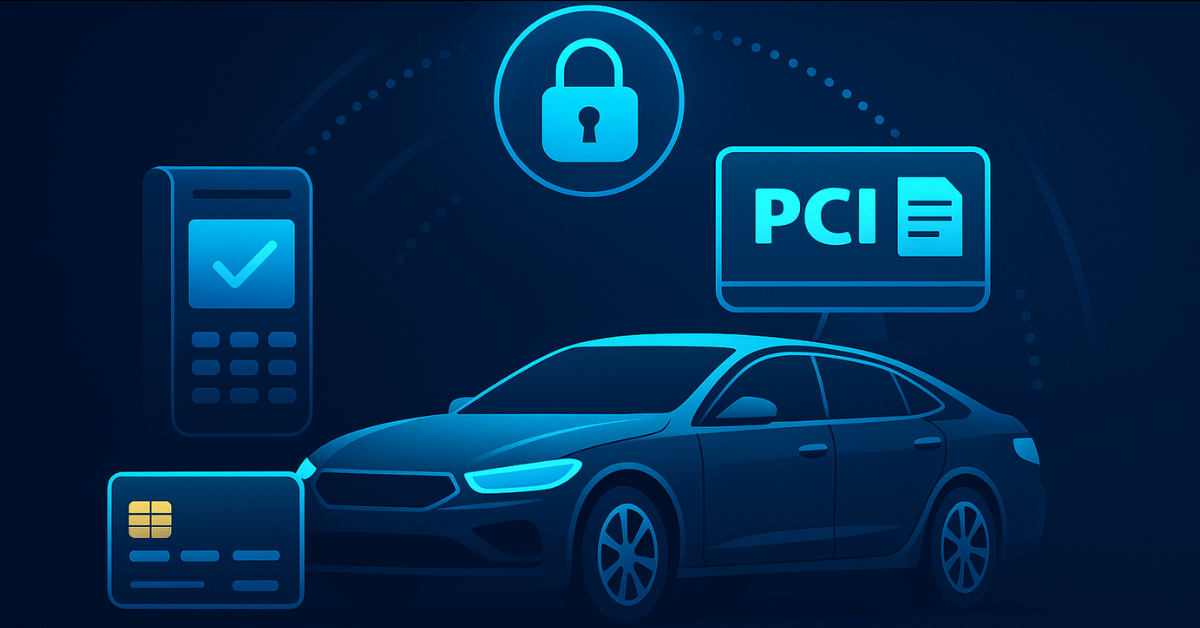

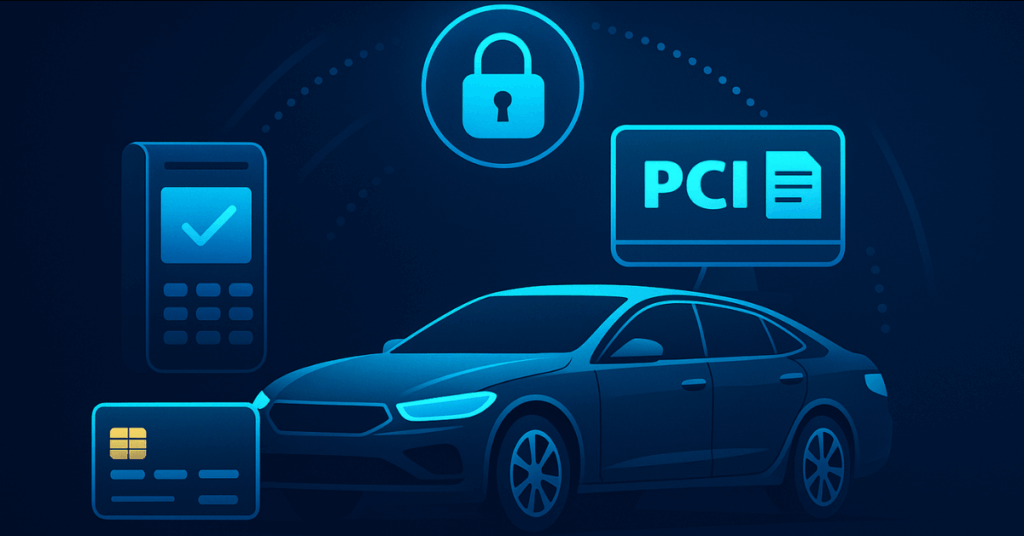

The Hidden PCI Risks of Connected Cars: Why In‑Vehicle Payments Need More Than Just a PIN

Connected cars are no longer just about navigation and entertainment. They are becoming mobile commerce platforms that allow drivers to pay for fuel, parking, tolls, EV charging, and even coffee directly from the dashboard without touching a wallet or phone. This convenience is reshaping how consumers interact with the automotive industry, but it also introduces a new and largely overlooked frontier for PCI DSS compliance and data security.

When payment data moves into a constantly connected vehicle, it changes the risk landscape dramatically. The car itself becomes a payment terminal on wheels, and with that role comes a range of security and compliance challenges.

How In‑Vehicle Payments Work

Modern in‑vehicle payment systems integrate a driver’s credit card, debit card, or digital wallet into the vehicle’s infotainment system. The car uses its built‑in connectivity, often over 4G LTE, 5G, or Wi‑Fi, to communicate directly with payment processors. Transactions can be initiated using a touchscreen, voice commands, or in some cases biometric authentication like fingerprints or facial recognition.

Manufacturers such as Hyundai, Mercedes‑Benz, and General Motors are leading the charge. They have partnered with payment processors, parking service providers, and fueling networks to create seamless payment experiences. Hyundai Pay allows drivers to pay for fuel, parking, and EV charging without leaving the vehicle. Mercedes Pay uses biometric authentication to authorize payments securely from within the infotainment system. These features are being marketed as both luxury and convenience benefits, but they also put vehicles squarely within the scope of PCI DSS if cardholder data is stored, processed, or transmitted.

Why PCI DSS Applies to Vehicles

PCI DSS applies to any environment that stores, processes, or transmits cardholder data. This means that if a vehicle’s payment system interacts with payment data, it must meet the same security standards as a traditional e‑commerce platform or point‑of‑sale system.

This can include:

- Ensuring that all payment data is encrypted while stored in the vehicle and while being transmitted to a payment processor

- Applying rigorous patch management to the vehicle’s infotainment and payment applications

- Conducting vulnerability scanning and penetration testing to identify and remediate weaknesses before they are exploited

- Controlling access to payment systems through strong authentication

Hidden Risks That Often Go Unnoticed

- Vulnerable Infotainment Systems

Vehicles are essentially complex IoT devices. If the infotainment system has an unpatched security flaw, attackers can exploit it to intercept payment transactions or access stored credentials. - Insecure Over‑the‑Air Updates

Automakers use OTA updates to deliver security patches and feature enhancements. If the update process is not securely designed, attackers can inject malicious code or block updates entirely. Delays in applying these updates can leave vehicles exposed. - Third‑Party Service Weaknesses

Many in‑vehicle payment systems rely on third‑party platforms for processing transactions or integrating location‑based services. A breach at one of these partners can compromise the security of the entire payment process. - Physical Access Threats

A malicious actor with temporary physical access to the vehicle, such as a valet or mechanic, could tamper with hardware modules or install unauthorized software to capture payment information. - Public Network Risks

Drivers sometimes connect vehicles to public Wi‑Fi networks for convenience. If payment transactions occur over insecure connections, the risk of interception increases significantly.

What Merchants and Service Providers Should Do

- Require that in‑vehicle payment integrations meet PCI DSS requirements and can be validated by the automaker or payment service provider

- Extend vulnerability scanning programs to cover vehicles if they are handling payment transactions tied to your brand or service

- Implement tokenization so that no raw cardholder data is stored within the vehicle’s systems

- Educate customers about the importance of keeping vehicle software updated and avoiding risky network connections for transactions

- Work with MSSPs and Approved Scanning Vendors to verify that payment systems are secure before they are deployed to customers

The Road Ahead

In‑vehicle payments are moving quickly from a niche luxury feature to a standard capability across multiple automotive brands. As adoption grows, the scope of PCI compliance will naturally expand to cover these systems. Organizations that embrace this reality early will be better positioned to protect customers, maintain compliance, and avoid reputational damage.

The convenience of paying from the driver’s seat is here to stay. The challenge for automakers, merchants, and service providers is to ensure that convenience does not come at the cost of cardholder data security. This means treating the vehicle not just as a car, but as a fully fledged payment endpoint that requires the same rigorous security and compliance measures as any other part of the payment ecosystem.

As a Managed Security Service Provider and an Approved Scanning Vendor, we help organizations integrate in‑vehicle payment systems into their vulnerability management and PCI compliance programs. This approach ensures that security is not an afterthought but a built‑in feature that protects both businesses and drivers.